Reimagining mortgage distribution

We create powerful software, data and analytics that unites lenders, brokers and aggregators to operate compliantly and efficiently, giving borrowers certainty earlier in their search for a mortgage.

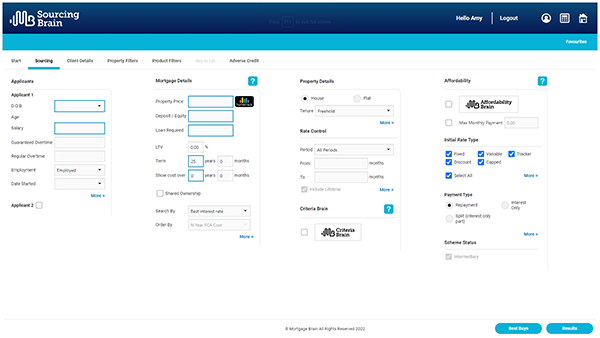

Our Integrated Solutions

With over three decades in the industry, Mortgage Brain is well positioned to reimagine the industry plumbing - the way mortgage products are sourced and distributed. Our mortgage broker software offers streamlined, simple, and efficient solutions for mortgage intermediaries, lenders, and business partners throughout the whole mortgage process.

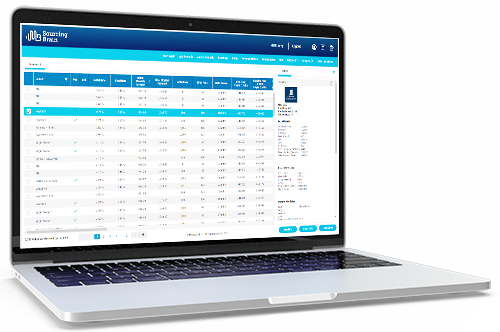

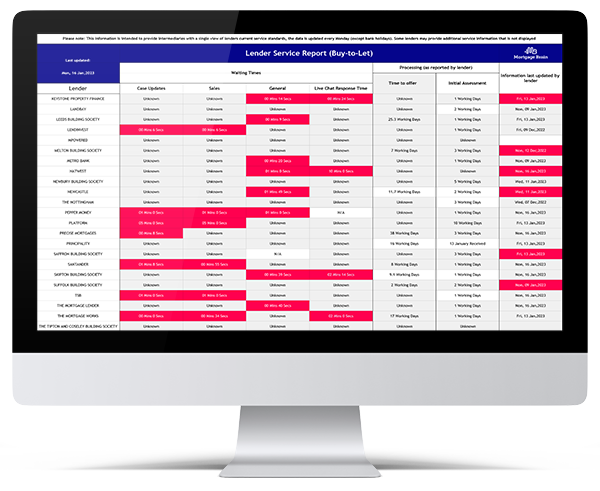

Lender Service Report

Whether you’re a mortgage adviser using our mortgage broker software or a lender, the Lender Service Report is a handy tool that is updated fortnightly. It’s a central point that gives a snapshot of the state of lender service levels across the industry. A quick look tells you the sort of waiting times you can expect for different aspects such as case updates, general response times, initial assessment, and time to offer for both residential and buy-to-let.

For mortgage advisers, it means you quickly make recommendations and set clear expectations without spending time visiting each lender’s website.

For lenders, it’s an easy way to gauge how your service levels are performing against those of your competitors.

Insights

Gain valuable industry insight with our up-to-date articles

testimonials

Stephen Brown | Head of Intermediaries

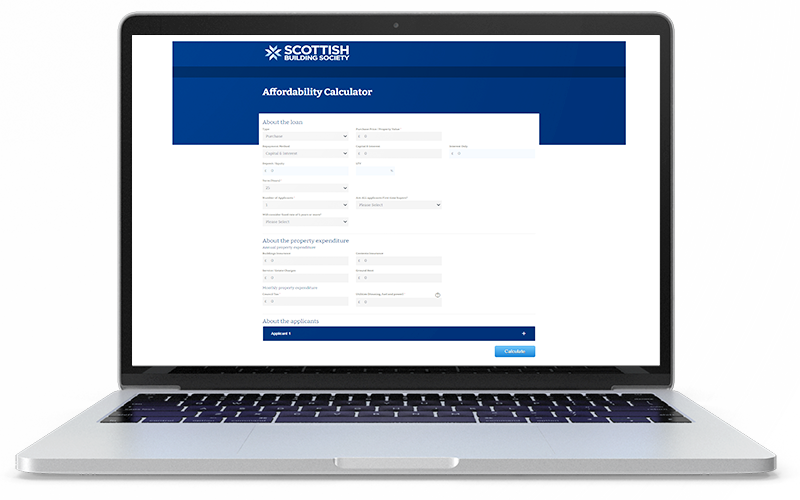

“Mortgage Brain helped us build our affordability calculator. It has greatly improved our broker journey and allows brokers to quickly compare us against a myriad of lenders.”

Sophie Waugh

“Mortgage Brain’s functions allow us to source deals, view lenders’ criteria, and check affordability making life as a broker so much easier. ”

MSS

Rob Clifford | Chief Commercial Officer

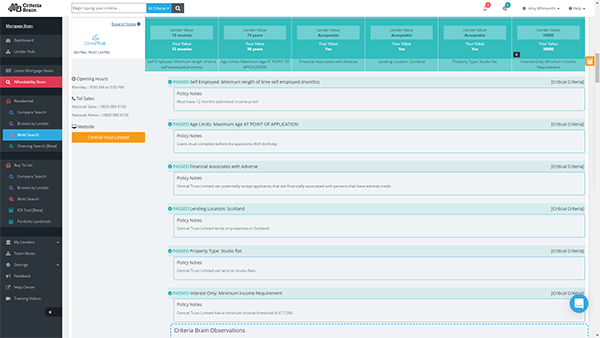

“In addition to Sourcing Brain, we also get access to Affordability and Criteria Brain which are incredibly useful tools and make it easier for brokers to find the best products with confidence.”

SimplyBiz Mortgages

Richard Merrett | Head of Strategic Development

“Mortgage Brain's excellent tools such as Criteria Brain and Affordability Brain help to narrow the funnel and guide advisers towards the best potential solutions.”

MSS

Carl Webber | Chief Technology Officer

“Changing our sourcing provider was a significant project for us, MBL's support team was brilliant and the collaboration on future developments is something that we very much value.”